How much do you know about credit scores, how they’re calculated, and what

they’re used for? Ramp up your knowledge with this helpful guide so you know

what to expect next time you apply for credit.

What’s the Score?

Your credit score is a part of the package of information lenders use to decide

whether or not they will lend you money or extend credit. Other factors

include things like your employment history and income and their own internal

scoring systems.

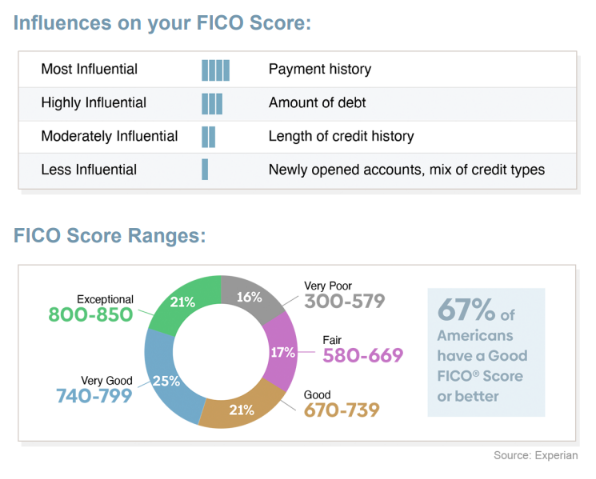

There are two primary credit scoring models you need to know about: FICO

and VantageScore. Each may be used to determine your creditworthiness:

that is, how likely you are to repay your loan. Your score can influence your

interest rate, length of loan, and even how much you can borrow.

Calculating Scores

Both scores use a range of 300-850. A higher score indicates to lenders that you

are fiscally responsible and the risk of lending to you is low.

What Will My Lender Use?

FICO is used by 90% of lenders, according to myFICO, and has been around

since 1989. (VantageScore only hit the scene in 2006.)

While the FICO Score is currently the gold standard of credit scoring systems,

VantageScore is extending its influence throughout the lending industry. Banks,

credit unions, credit card companies, mortgage lenders, and more continue to

increase their use of VantageScore. In addition, landlords and some government

agencies also use VantageScore.

If you’re not sure which scoring model a lender will use, just ask!

Are you are interested in seeing how your current credit score might affect a new mortgage? Call Crown Mortgage Company at 708-857-1897.